Supply Terminology

When a firm supplies a good or service, then you assume 3 things:

- The firm has the resource and technology to produce it.

- The firm profits from making it.

- The firm is definitely making it and selling it

The quantity supplied of a good or service is the amount that producers plan to make and sell during a time period at a specific price.

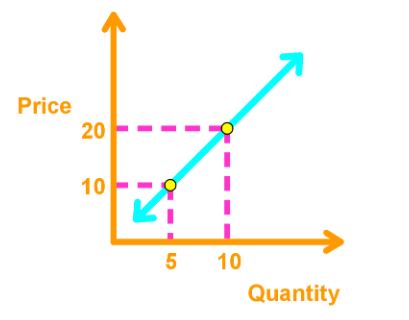

Law of Supply and Supply Curve

Law of Supply: the higher the price of a good, the bigger the quantity supplied. This also happens vice versa.

The supply curve function is = a + bP, where

- P is the price of the good or service

- is the number of quantity supplied

Note: The supply curve is the same as the marginal cost curve we’ve seen last chapter.

- Increasing Opportunity Cost: The higher the price, more firms are willing to produce and sell because any higher opportunity costs can be covered by the higher price. Thus, more products are supplied.

- Rising Marginal Cost: the more units are produced, the higher the marginal cost of production. So firms need to make sure that the extra addition unit cost is covered by the higher price in order to make profit.

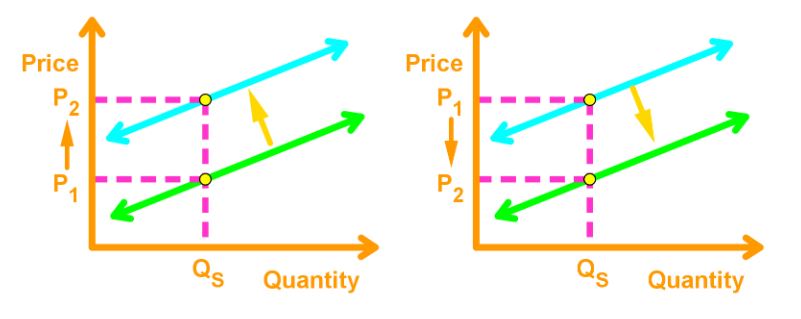

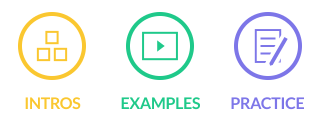

Change in Supply

The supply curve can either shift rightward or leftward. Reasons why supply curves can shift:

- Prices of Factors of Production: if the prices for factors of production increases, then it becomes more costly, causing producers to produce less of the supply at the price. This shifts the supply curve to the left.

- Prices of Related goods produced: prices of related goods which firms make influence supply.

- Substitutes: Suppose good x and y are substitutes. If the firm is producing good x, and the price of good y increases, then the firm switches to good y, causing the supply of good x to decrease.

- Complements: Suppose good x and y are complements. Then increasing the price of good x will increase the supply of good y.

- Expected future prices: If the price of a good is expected to rise in the future, then the supply of the good today decreases. This causes the supply curve to shift leftward.

- Number of Suppliers: The more supplies there are, the greater the supply of the good. This increases the number of supplies, which shifts the supply curve right.

- Technology: Advancement in technology lowers the cost of producing, which means suppliers will produce more of the product. This shifts the supply curve to the right.

- State of Nature: Any natural disaster that can influence the production, or damage the supply will lower the amount of supply. This decreases the amount of supply, which shifts the supply curve leftward.